Over the next month, Helen and Sarah are focusing on Squiggly Careers ‘life skills’. They will be covering health, sleep, money, and relationships and understanding the practical actions you can take to create the strongest foundations for squiggly career success.

Today, they are talking about money and borrowing some brilliance from Morgan Housel, author of The Psychology of Money, and author of You are a badass at making money, Jen Sincero.

Ways to learn (even) more:

1. Sign-up for PodMail, a weekly summary of squiggly career tools

2. Read our books ‘The Squiggly Career‘ and ‘You Coach You‘

00:00:00: Introduction

00:01:04: Books behind this week's episode

00:03:18: What Helen learnt from her book…

00:03:21: … 1: being rich vs being wealthy

00:04:45: … 2: saving vs spending

00:09:26: … 3: money buys you freedom and flexibility

00:10:46: What Sarah learnt from her book…

00:11:24: … 1: a complicated relationship with money

00:14:31: … 2: examining your feelings around money

00:16:49: … 3: what a spreadsheet says about you

00:21:23: A scale of watchful to wasteful

00:23:35: Taking accountability for good money management

00:24:45: The target market for the books

00:27:03: Standout quotes from the books

00:28:37: Final thoughts

Sarah Ellis: Hi, I'm Sarah.

Helen Tupper: And I'm Helen.

Sarah Ellis: And this is the Squiggly Careers podcast. In the next few episodes, we're doing something a little bit different. We're focusing on some of the factors outside of work that we think will help you to succeed in work, and the topics we're covering are health, sleep, money and relationships. We're absolutely not the experts in any of these topics, so we've decided to choose a different book to both read; and in our conversations together, we'll be talking about what we've learnt and how it's helped us, and hopefully how it might help you too.

Helen Tupper: You realise, Sarah, that our work should be transformed by the end of this series?

Sarah Ellis: I mean, let's maybe wait until after today's conversation before whether we decided whether that's true or not, because today we are focusing on money. And I think it's fair to say that of all of the four topics, we have found this one quite tricky to discover the right books that we thought were going to be helpful for everybody listening. So, Helen, do you want to talk to us a bit about what book you have ended up choosing and why?

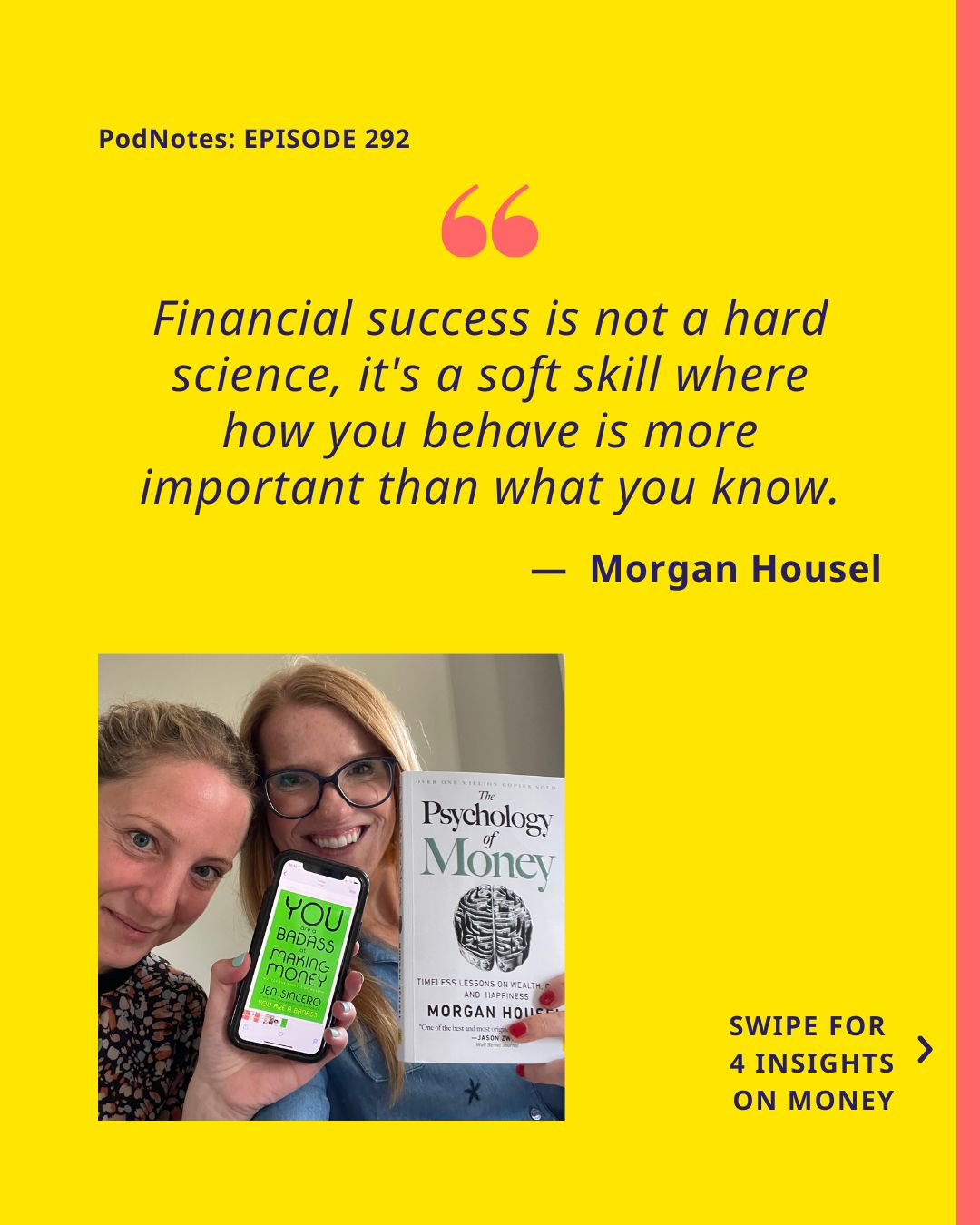

Helen Tupper: Yeah. I started and stopped with a few and I was like, "This isn't useful; this isn't useful", and I ended up with one that was interesting. I've had to work quite hard to make it useful, but I didn't think I could pick up and put down another book on money. So, I've gone with a book that has had, "Over 1 million copies sold", it proudly says on the front, The Psychology of Money: Timeless Lessons on Wealth, Greed and Happiness, by Morgan Housel.

Sarah Ellis: So, similar to Helen, I started and stopped quite a few different books. Now, I do want to give a shoutout to one book that I did read; it just didn't quite work for our podcast format, but was a useful read, and that was Money: A user's Guide, and that's by Laura Whateley. I've seen it in loads of bookshops, it gets really good reviews and ratings, and I think as a practical guide to finance, it is really helpful. It will tell you what an ISA is, it will explain how renting works. But it's almost so relentlessly practical, unless I was going to come on the podcast and talk to you about ISAs and savings, it didn't really feel like it was going to work.

But that was a useful book on money, and I have recommended it actually to a few people; I think perhaps particularly if you are starting out. It's one of those books you think, "I wish I'd read that in my early 20s", because I think Laura's own experience with money as well, she reflects a bit on that, but it is a really good practical guide. Then I read a few others that I really did start and stop and thought, "This is not very useful", or was going in lots of different directions. And then I thought, "I'll pick a book that I would never normally read", because I think this series is an opportunity for us to do something a bit different.

So, I read a book called, You are a Badass at Making Money, by Jen Sincero, and her books have sold lots and they get incredibly good reviews, thousands and thousands of reviews, but it is not a book I would have ever picked off the shelf. I think the title would have perhaps put me off, if I'm honest, and even how it's described. I was like, "This doesn't feel like something I would normally spend time with". But I think it's good to challenge your assumptions.

Helen Tupper: You challenged yourself, your growth mindset was in action.

Sarah Ellis: It was, and I thought, "Okay, I've not really read very many books on money, so let's see, and then let's see if I think this would help me with me and my career". So, shall we dive into, "What have we learnt about money?"; do you want to go first?

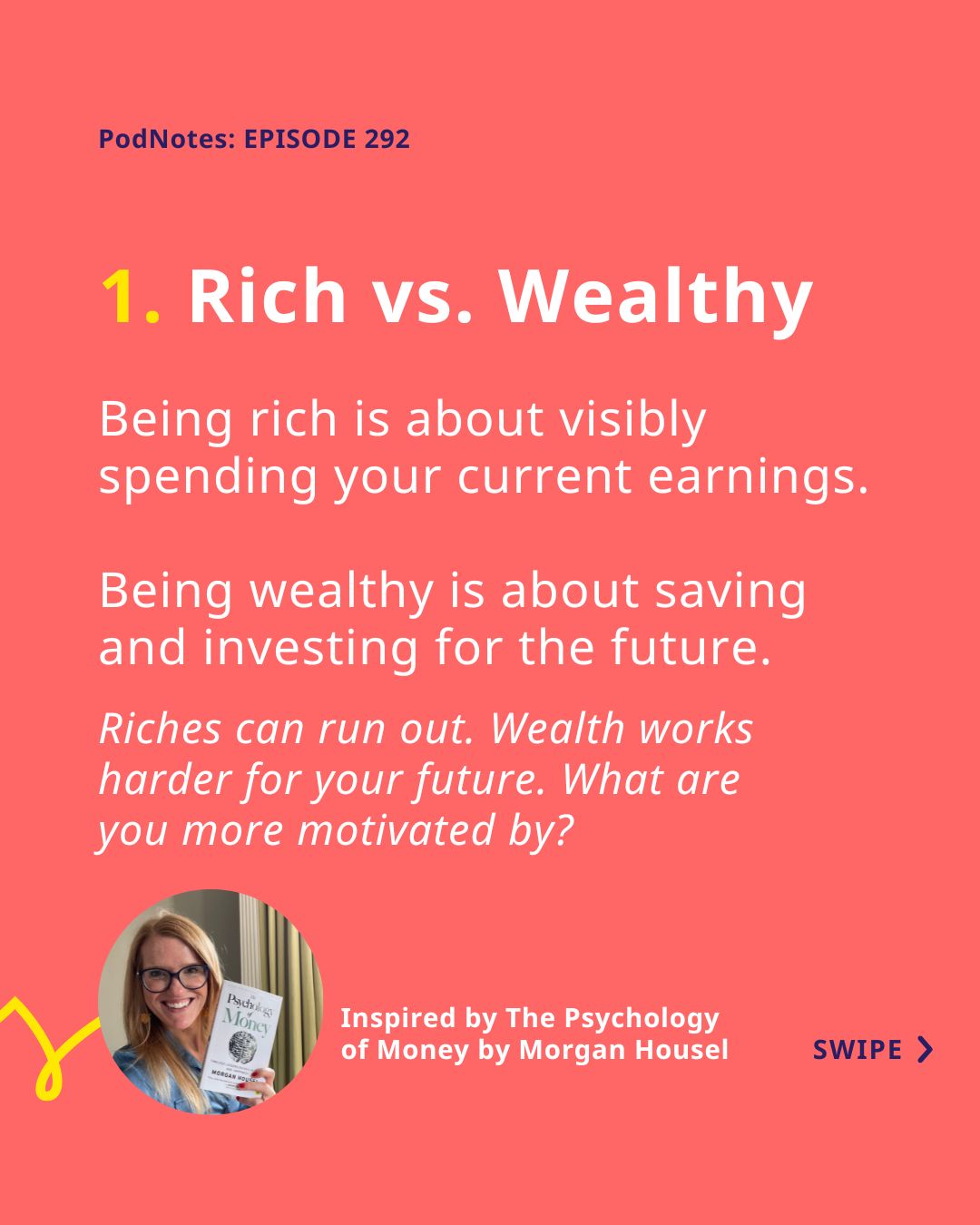

Helen Tupper: Yes, okay. So, bearing in mind mine is a bit more psychological, given the nature of the book, the first thing that I learnt: being rich is different to being wealthy.

Sarah Ellis: Tell me more?

Helen Tupper: I'll tell you more. Okay, so I've written down, "Rich equals your current income", so, "Cash and flash", is what I wrote down. So, your current income, your ability to take yourself out for a nice dinner, to buy yourself some nice clothes, if you can afford to do that, you are rich today. But that is different to wealthy, because in the book he says that wealth is hidden; so, it's not cash that you flash, it's the stuff that you can't see. It's basically income not spent. So, you have that money, but you are choosing not to spend it.

Sarah Ellis: So like savings?

Helen Tupper: Well, yes, and we'll get onto savings; my second thing I learnt was about savings! But I thought that was quite interesting actually, just to distinguish between, just because you see somebody -- let's say you see someone who's got lots of things, you're like, I don't know, they always dress really well or they've got a nice, I don't know, they look nice or they've got nice things, that might mean that they've got a lot of current income, but that is different to someone who is wealthy, because the point in the book is that actually, someone who's wealthy has money that you can't see. It might be invested, or it might be saved. And actually, over the longer term, wealth is what matters.

Sarah Ellis: Okay!

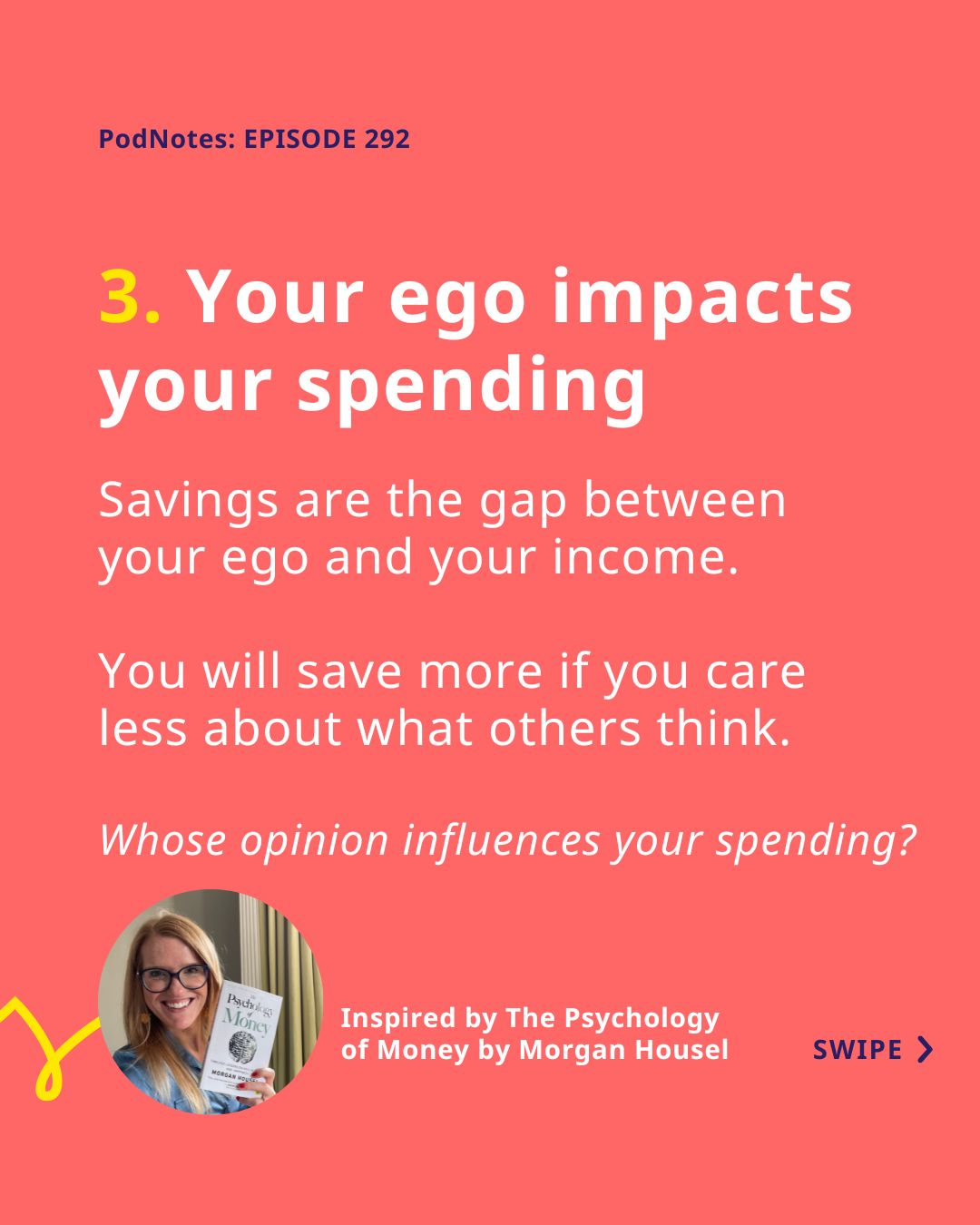

Helen Tupper: So, that was the first thing, I thought that was an interesting to reflect on. Onto savings, Sarah, there you go, "Savings are the gap between your ego and your income", which I liked!

Sarah Ellis: Oh, tell me more!

Helen Tupper: There was a nice little quote in the book that says, "Savings can be created by spending less. You can spend less if you desire less; you will desire less if you care less about what other people think", which is where that ego bit comes in. I thought that was really interesting, like how much of your spending is driven by something that you want to acquire because it will influence what other people think of you?

I don't think a lot of people would admit that, but are you dressing nicely because it makes you feel good, or because it's to fit in with other people, or it's what's expected of you in a certain group; or are you buying a new car because your friends have, or is it because you generally think it's going to get you to another place more comfortably off. That kind of stuff I thought was interesting; savings are the gap between your ego and your income. What do you think about this statement?

Sarah Ellis: I was just trying to think about anything that I spend money on that feels more ego-related, because I think I'm more of a saver than a spender. What would you describe yourself as?

Helen Tupper: You know the answer to that! I was reading this with two different -- so, Sarah and I are super-different with money, and I am definitely more rich, and Sarah's more wealth, I would say, based on what we've got to, because I do like buying things. I don't know whether it's ego-driven though. It did make me question; I just really like nice things and I like nice clothes and nice watches and nice things. Sarah and I have known each other 20 years, and that has always been me, I've always been that person.

Sarah Ellis: And I was just thinking, do you know what, I was thinking more about you when you were talking about ego that I was about me, because I was thinking I'm not sure your purchases are driven by ego, I think they're driven by enjoyment!

Helen Tupper: Yes, I think they are too! I just like a new bag and I like it all. Although it did make me think, I'm considering buying a new watch and I was like, "But am I buying this new watch for ego, or am I buying it because I just like a new watch?" and it's really made me pause on my decision to purchase!

Sarah Ellis: I think that's one of the things, you and I were together yesterday and we were talking about some of the challenges of finding useful books on money, but we were both saying almost the process has encouraged us to reflect on our relationship with money. And it did remind me that when I was younger, I used to have -- you know when you go to a bank, they give you the little bags for putting money in?

Helen Tupper: Bags?

Sarah Ellis: The little see-through, small bags.

Helen Tupper: Oh, the little plastic ones? I thought you meant some kind of -- how much money did you have? Like some tote bag or something!

Sarah Ellis: No, you know the little, small ones that you get; well, I used to when I was younger.

Helen Tupper: Yeah, to count your pennies.

Sarah Ellis: Yeah, so I used to save up 5ps and 10ps and 20ps from my pocket money or money that I'd got, and I would keep all that money. I've got quite vivid memories, now that I've thought about it, almost like hoarding, and I just quite liked it. I liked seeing it grow, and I'd not even got anything specific that I was saving for, which I thought, "That's quite interesting". It wasn't like I was motivated by, "I'm saving up for this magazine", as a kid or, "this top that I want to buy"; I just liked the, "That feels good that I have saved that money".

I wonder whether that probably says quite a lot about you in terms of your relationship with money, like maybe I'm assuming a bit probably how you grew up, what your parents were like, but that I've probably always slightly been more of a saver.

Helen Tupper: It's so funny, I was just thinking about children, and I went for a walk this weekend with my children; and my daughter, Madeleine, we were walking in a forest, and she decided this was a great time to wear a pink mouse bag, which I didn't realise she'd got. Anyway, we were walking in the forest and she's got a pink mouse bag on and it's jangling as she was walking. I was like, "Madeleine, what's in your bag?" "Money, mummy". I was like, "Okay, she's 5". I was like, "What money?" And she's like, "All the pennies. Do you want some money?" And literally for the rest of the walk, she was like, "Do you want some money?"

She decided to take a bag full of pennies on a walk in a forest in a pink mouse bag, and then she was just wanting to give some away, and I was like, "That's probably a bit like me being, 'I've got it --'" I always used to be, when I was younger, this is where I think we're different; I would always go on holiday with my dad and I would have some spending money for this trip, and we used to go to National Trust properties all the time. It was the Three Cs holiday: castles, churches and cathedrals always featured in a holiday with my dad! I would go to the National Trust shop with my £2, or whatever I was given, and my mission would be to spend every single penny. I mean, there was no saving going on when I was 5 or 6, so yeah, I think we might have some differences, Sarah, possibly.

My last learning that I have noted down was that, "Flexibility and control over your time is an unseen return on wealth". The point in the book is that yes, money can buy you things, fine; but actually, one of the biggest things that money, so savings, can buy you is freedom and flexibility, and people don't necessarily consider the value of that, because it's perhaps a bit intangible. But it gives you choices, and I just think very much about what that has enabled us to do.

So, when Sarah and I started our business over ten years ago, we saved all of the money. I mean, in the beginning, it didn't really make a lot, but every little bit it made, we saved. It meant that when we were considering leaving our corporate roles, seven years on from when that business started, and we were considering leaving our corporate roles, because we hadn't spent the money that had accumulated during our work on our side project over seven years, suddenly we had this choice of, "Okay, one of us could leave our corporate job, and we've got a six-month financial runway to see whether we can turn this side project into a viable business that could actually pay us both a salary".

We wouldn't have had that flexibility and that freedom had we not saved those funds, so I think I really related to that point in the book when I read it.

Sarah Ellis: Also, what is interesting is you and I have a very different, I think, personal approach to money; but from a business perspective, we don't argue about money ever. We argue about other stuff, or have heated debates, or whatever we want to call them, whatever I'm meant to more positively call them! And there are other things that I think we definitely disagree on, but actually money has never been a challenge for us so far, which I do think is interesting, given we have different personal starting points, and maybe that's because we're aligned in what we're trying to do and how we want to do that; I don't know, but I do find that interesting.

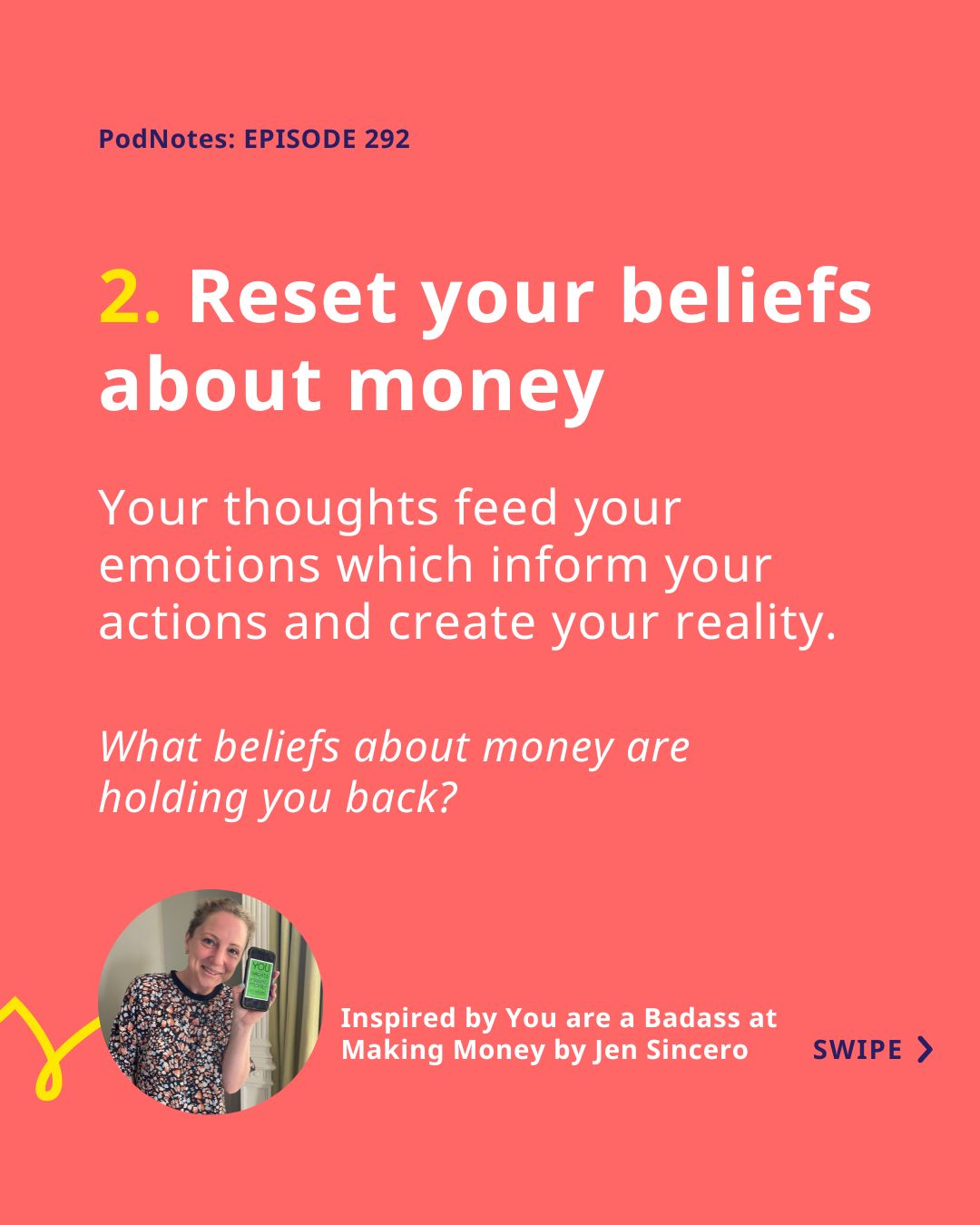

So, a couple of things I learnt from the book. The first one was around the complications in terms of our relationship with money. Money is something that we don't talk about, lots of people don't talk about, and it can cause friction. One of the things that Jen says is that the beliefs that we have, and sometimes these beliefs are sometimes quite limiting, really impact our relationship with money. So, she uses this equation where she says, "Your thoughts inspire your emotions, which inspire your actions, and then that forms your reality".

Her argument is that sometimes, we are very attached to the unhelpful familiar, which is her starting point to why you might stay in a job that feels very safe and secure, because you'd be worried that, "Okay, well if I did go to run my own business, or I did try to do something different, what are the financial implications of that?" and we're always happier with what we already know. It's sort of about our relationship a bit with uncertainty.

I was thinking about, I think, for me with a money perspective as I've got older, as I've grown into an adult, away from my 5p money bags for a kid, I do think I've got some limiting beliefs around money, because I wasn't very good at maths at school. So, because I actually think from a thought perspective, I always think I'm just not very good at numbers, I think then my emotion is, "I'm nervous about money". I get quite nervous about, "I don't think I understand, I don't think I would be able to make good decisions". And then, in terms of the actions that that inspires, I think that makes me very cautious and it means that I would always play it very, very safe in terms of the money that I've got.

So, I hate the idea of losing money that I've earnt. So, you know, I'm sure, you should invest to make good returns, or whatever, and I've got friends who do that, who almost quite enjoy maybe dabbling with buying some stocks and shares, which probably the way I'm describing this shows just how little I know about this, but --

Helen Tupper: Put some money into these investment portfolio things!

Sarah Ellis: Yeah, which tells you everything you need to know about my finances! But you know the idea -- I also worked in a bank, I worked for Barclays! But you always get that disclaimer with your investments, "Your money can go up and down, and you need to be aware of that". I was like, the idea that money that I have worked hard to earn could diminish, could go down, I find that really difficult to get my head around.

I also get that then there's a really big upside, that you could invest in something that there could then be really big rewards. But you know that risk/reward thing? It really made me think, I am quite risk-averse, it's why I don't have loads of savings, and Helen and I talked about, we need to sort our pensions out, and all those kinds of things. We are definitely not role models at all when it comes to money. But from reading the book and thinking a bit more about money, it definitely made me think about, "What are the beliefs that I've got that might sometimes get in my way around money?" So, I found that quite interesting.

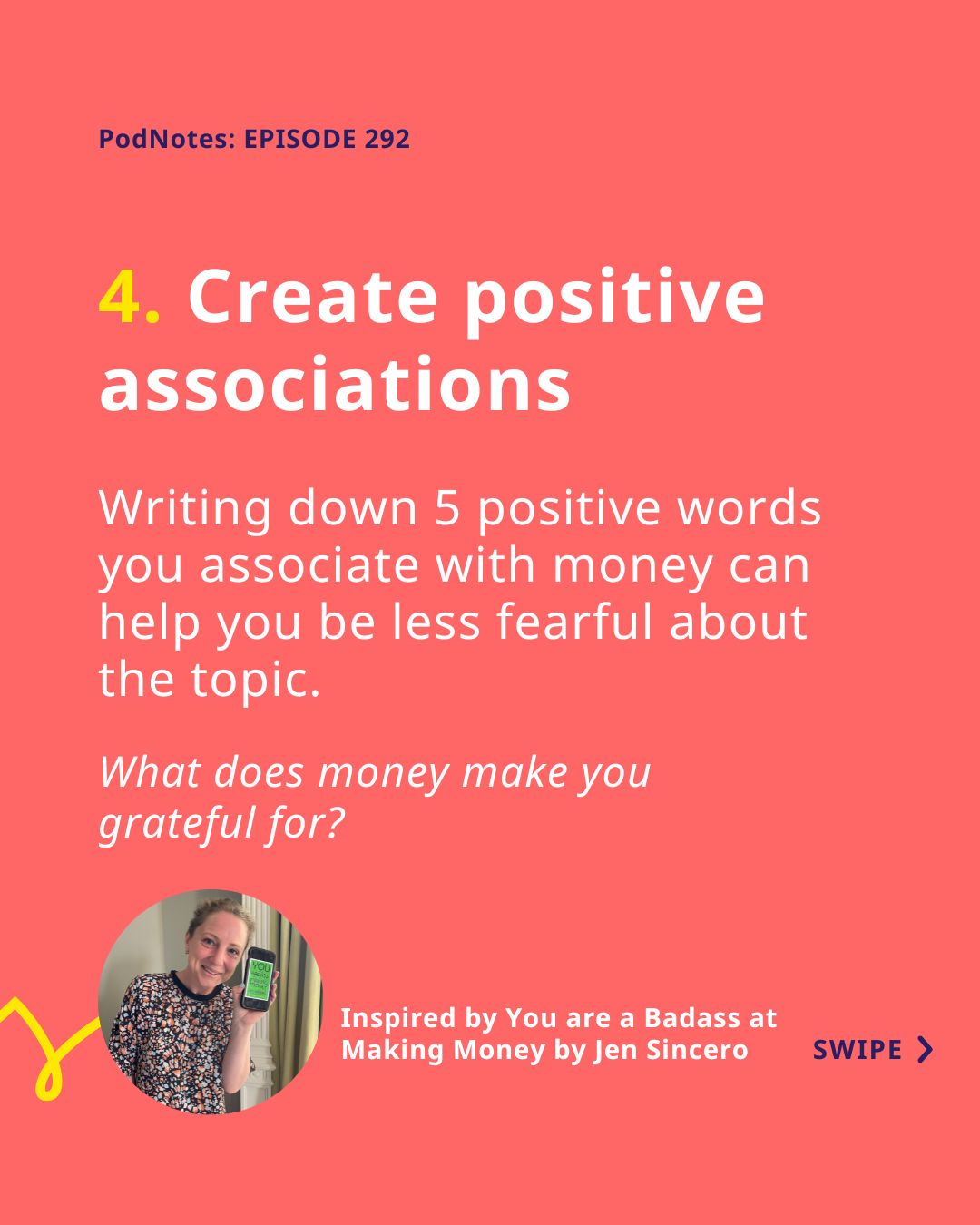

As you go through the book, there are some questions and exercises that I did find useful to consider, so one of the questions was, "Write down five positive words to describe money", and I was like, "That's quite interesting", to see what words you would write down. So I wrote down, "Opportunity, presents, freedom, experience and food"!

Helen Tupper: Nice.

Sarah Ellis: Because I was like, I actually think that's a good exercise. It's kind of, what does money mean to you?

Helen Tupper: And especially now you talked about feeling nervous about money; I think those words could help you to create a more positive association with it.

Sarah Ellis: Yeah, which is exactly what I think Jen is encouraging you to try to do. And then, almost finish this sentence, "I'm grateful to money because…" So, you know if almost you're not sure how you feel about money, or perhaps you worry about -- you know sometimes you feel a bit uncertain about having money, or maybe apologetic about money, so what is good about money, why it's a good thing, we should try and have a good relationship with money.

Then one of the other things that I like that she suggested, the book is very into manifestation and visualisation --

Helen Tupper: Your favourite thing.

Sarah Ellis: -- which I found challenging at times, I think it's fair to say; we'll come onto that. But one of the exercises which I do think could be helpful is to do a, "What you would like a day in your life to be like", so almost be really specific. I think that's quite a fun exercise. You might do one version of a day in the life that doesn't feel too far away from where you are today, and maybe you do one really ambitious one. And so, you do a couple of those, and then you ask yourself the question, "What does that mean in terms of money?" and, "What does that mean in terms of finances?"

So, if that is a day in the life that I'm really motivated by, or that I'm working towards, what does that mean that I would need to do, or the decisions that I might need to make? One of the points that she does make is, "If you want to change your finances, you have to be prepared to make changes". It's not just going to happen, you have got to proactively got to make some choices and decisions. So, I thought those were some useful things, as I went through the book.

Then my final thing is something a bit different, and it's cheating. So, I ran out of things from the book.

Helen Tupper: Never a good sign!

Sarah Ellis: And then, I listened instead to an episode of TED Business, called The Emotions --

Helen Tupper: This is such a cheat, Sarah!

Sarah Ellis: Sorry!

Helen Tupper: Right, so you ran out of three things?

Sarah Ellis: But it's really good, this is good.

Helen Tupper: All right, this is like an extra bonus from something else?

Sarah Ellis: It is. So, this is the TED Business podcast, and it's called The Emotions Behind your Money Habits, and it's a guy called Robert A Belle, he's an accountant. It's really short, you listen to it for like 13 minutes, and I really enjoyed listening to that, I found it helpful. He talks about how basically, your relationship with money reflects your relationship with your life, and how a spreadsheet can actually tell a story about who you are and what's important to you.

Almost by coincidence, I didn't know this was what he was going to talk about, me and my partner have actually been through this exact exercise really recently. So, what you do is, you do a spreadsheet where you say, "Here's everything I've spent in the last six months", and you categorise it. There are even some banks and apps that do this for you, so you'll be like, "I spent this much on food [or] on health [or] on fun stuff", whatever categories you want to come up with.

Then you view that spending with an inquisitive and curious mind, so you're not trying to blame yourself or beat yourself up; you're just trying to look for patterns and ask yourself, is there anything you are shocked or surprised by. His point is, sometimes our money knows us better than we know ourselves.

Having done this exact exercise really recently, prompted by my partner not working at the moment, so we were going, "We need to think about our finances and do a bit of rejigging, certainly in the short term", we actually did this and realised that we spent way more than we realised on takeaways.

Helen Tupper: That doesn't surprise me, you're always having a takeaway!

Sarah Ellis: Not anymore, not since the old spreadsheet came into life!

Helen Tupper: Are you cooking more now?

Sarah Ellis: Well, when you say me, I mean I'm not cooking more. But his whole point is, it's the difference between avoiding versus being accountable. So, I would have always said, "Oh, yeah, we definitely get a few takeaways. I love food, that feels --" I'm not going to apologise for that, that's something I really enjoy. But when you do the spreadsheet, I was surprised by the frequency and just the number, as in the amount of money you're then spending on that thing. Basically, Deliveroo is making a lot of money from my house.

Then you ask yourself, "Okay, so why is that?" Is it because you're having a particularly busy week, is it because you're stressed; are you doing it when you're stressed and when you're celebrating? It's interesting to see what are the behaviours that are driving that spend. And then thinking about, "Do you feel good about that; does that make you feel proud about spending that money? Or, is there something you want to try doing differently?"

I think the reason I liked listening to him was it felt really practical and it felt very doable. And having done it, and that was a pure coincidence, it's meant that things like, we still get takeaways, because I love getting a takeaway, but we probably get 70% less. We probably get one every week, or one every other week, and suddenly you spend a lot less, and then I feel good about that. Or you realise things like, recently I was actually telling Helen this this week, I realised I was spending twice as much on my internet as I probably should be.

It prompts you to just re-evaluate how you're spending your money, but not in a way that made me feel bad; in a way that actually made me think, "I'm going to do something about that, I'm going to take that accountability". So, it's quite a simple thing, and I'm sure some people listening are probably already very on top of this stuff and have done it before. I certainly hadn't; I hadn't looked at my money in this way, and I think then you can -- my partner, I have to say, is an accountant, so this spreadsheet that we have created is incredible. I'm also not allowed to touch it, because I might mess up the -- I think there are formulas and all sorts!

What's interesting is my partner just enjoys the process of the spreadsheet. I think I enjoy the "so what?" of the spreadsheet. He actually enjoys creating it and tracking it, but I'm not sure if he'd necessarily do anything that differently. Whereas I go, "That's really interesting. I think I could spend a bit less on Amazon, or I could spend a bit less on takeaways, or I could reduce my internet and still get the same broadband that I need". So, that's been a very practical thing that I can personally say has been really helpful for me. And then listening to that podcast, I was like, "That's him reenforcing something that I have experienced as being really, really helpful".

Helen Tupper: You know I love a scale and a matrix?

Sarah Ellis: Obviously.

Helen Tupper: And listening to you makes me think about a scale, where on one end of the scale, you've got "wasteful", and on the other end of the scale you've got "watchful". I was listening to you and thinking, "I really don't think I'm very good at managing money at all", and I think that I avoid, to your point, I actually avoid looking at it. So, I would very rarely go into my bank account, because I'm like, "Oh, gosh, there's loads of stuff that I probably should stop subscribing to", or, "I've probably done way too many top-up shops in a week", you know those ones where you incrementally spend more, because you're doing lots of top-up shops?

It makes me think, probably if I was to look at a scale at the moment between wasteful and watchful, I'd be much more towards wasteful, because I avoid looking, because I think it's almost a bit scary! But I think if I could become more watchful and almost think of one small change a week, and maybe that's too frequent; or, one action from Money Management a month, love the alliteration, but I think I could make some incremental improvements.

Spending loads of time in my bank balance and completely changing the way I live and spend feels a bit daunting, but thinking, "Is there one subscription that I could cancel? Is there one top-up shop that I could stop?" one small action a week, or something like that, I think over time, I could probably become more watchful and less wasteful. But I think a radical change overnight just makes me think, "Oh no, I'll just do that another day".

Sarah Ellis: Yeah, I think that's a good way to view it. It is interesting, because we've been thinking about this topic for three or four weeks, and I think because it has been a hard topic to find books that we could both really connect with on, but I have spent quite a lot of time thinking about money. So I mean, lots of companies are not as well off now because of this, because I have probably changed or cancelled or realised that I was spending money in certain places, exactly to your point, that was wasteful, and it's really been a prompt for me to do something about that.

So, that's probably what it's made me do differently. So, reading Jen's book, listening to the podcast, reading some of the books, and even reading Laura's book which, like I say, described in very simple terms to me some things that I probably didn't understand that well, just made me start to go, "Am I being as accountable as I could be with my money?"

It also made me think a bit about who do I admire in terms of how they not necessarily spend their money, but almost manage their money. And I've got a couple of friends where I feel they're really on top of it, they're very organised and they've got a really positive relationship with money, they would talk about it very openly; not in showing off as in, "I've got loads of money", but as in they're confident about, they have taken that accountability, and then I see that in just how they describe the decisions that they've made that are right for them; and I admire that.

There is a book actually in Jen's book about, your relationship with money is also impacted by the people you're spending time with right now, as well as the people you grew up with, and I have got a couple of friends where I was like, "I think they do this really well already", and I think previously I've discounted myself and gone, "But I couldn't do that, because that's just not me", back to beliefs that can get in your way. Whereas now, I've challenged myself to go, "Why couldn't that be me?" and is that actually just about taking that bit more accountability and just feeling a bit more proud about how I manage my own money.

So, who would you recommend the book that you read to, Helen?

Helen Tupper: I think, as long as you're not looking for quick tips, so if you want quick tips, this isn't the book for that, because you have to work very hard to get something useful from an action perspective out of it. But I think if you have got a bit of time to think about money, and you want to think about your relationship with money, it's actually got a nice couple of stories in there. It slightly weights it towards Warren Buffet; there's a lot of Warren Buffet and there's a lot of Bill Gates references in the book. But if you want some stories to bring it to life, if you've got some time to think about money, I think this is a good book.

If you want to take action, I think if you're already in the headspace of, "I need to do something different", this probably isn't the first book to read. But if you're just thinking, "Maybe I could do something different with money, maybe I'd like to improve my relationship with money and understand it a bit more", and you've got the time to reflect on it, that is who I would suggest this book to. What about yours? That's a long pause!

Sarah Ellis: So, I think if you like the title of this book --

Helen Tupper: And, repeat it, Sarah, because you said it so positively.

Sarah Ellis: You are a Badass at Making Money.

Helen Tupper: Sounds great!

Sarah Ellis: So, if you like the sound of that title, I suspect you might like the book. If you are very onboard with the word "awesome", and manifesting and visualisation --

Helen Tupper: I'm so proud of you for reading this book!

Sarah Ellis: -- I think you might enjoy it. There are some useful things in there, but they are repeated, I would say, quite frequently, and I did have to work quite hard to get through the book. And not every book is for everybody, and this just wasn't a book for me. But as we have talked about, I think there are some -- because, it has prompted me though to think about money and my relationship with money, how I've grown up thinking about money, where I am with money today, and so I'm really glad that we chose it as a topic, because again, I really enjoyed listening to that TED podcast, which I would recommend to everybody. It's just a really interesting 13-minute listen.

So, spending some time, I think, thinking about money in relation to the work that you do, how you're living your life, is a useful thing. Whether this book is the right thing to help you do that, I think will be very personal to you and whether you like those styles of books.

Helen Tupper: And so, a quote then, Sarah, from the book that you worked very hard to read; did any particular statement or sentence stick?

Sarah Ellis: Yeah, there was one, which this one sentence I do really like.

Helen Tupper: Is it that you're an awesome badass?

Sarah Ellis: Absolutely not! It was, "Because we are creatures of habit who tend to have our words on repeat, they become like a chisel that forms grooves in our minds, playing the same stories over and over, anchoring in our thoughts and beliefs and defining our reality". I think that one, if it had just been that one sentence, that would have been really helpful for me, that book!

Helen Tupper: Also, I think that the way you read it, it gives a gravity to that quote as well. So, maybe if you read the audiobook, if you were the voice for the audiobook, it might give it that gravity behind the awesomeness.

Sarah Ellis: I mean, I don't want to read that audiobook!

Helen Tupper: Sarah is not picking up that monkey! My quote, see what you think about this one, "Financial success is not a hard science, it's a soft skill, where how you behave is more important than what you know".

Sarah Ellis: I like that.

Helen Tupper: I like that.

Sarah Ellis: Yeah, and it gets you away from, you know I said to you I think I've got a bit of a fixed mindset sometimes about my ability with money, whereas that suggests it's not about that.

Helen Tupper: Yeah, it's thinking about your behaviours, why you're spending, why you need to do that, what's driving it, rather than, "Do you know the current interest rate, or APR that you're paying on a credit card?" type stuff. You don't have to be an expert, it's more about your experience and your beliefs around money, which actually even though those two books are very different, I think is something that connects the two.

So, what we will do is, we will create a PodSheet for you, everybody, that has a summary of some of the things we've talked about, some of the bits that have really helped us and made us think differently, some of those questions that Sarah shared as well, if you want to do some money visualisation, or get a more positive association with money. They're actually definitely actions I'm going to do, I like those ones.

You can download that PodSheet from the link on the show description, which tends to be on Apple Podcasts, or you can just go to amazingif.com, our website, and you'll be able to find that. If you ever can't find any of our resources, by the way, it's just helen&sarah@squigglycareers.com, and we'll send them to you. You can also sign up for PodMail, which is a weekly email, which curates it all to make it super-easy for you as well.

Sarah Ellis: So, thank you all so much for listening, and we'll be back with you again soon. Bye for now.

Helen Tupper: Thanks everyone, bye.

Get our weekly insights, inspiration and tools sent straight to your inbox.